Climate related disclosures related disclosures are rapidly becoming essential in both global and domestic reporting. New Zealand has taken a leading role with the introduction of the Aotearoa New Zealand Climate Standards (NZ CS 1–3). This is a mandatory framework for reporting climate-related risks and opportunities, effective 1 January 2023.

These standards support consistent, comparable, and decision-useful reporting, equipping businesses and investors to better manage climate-informed strategies.

What are the NZ CS?

Developed by the External Reporting Board (XRB), the NZ CS standards establish a structured regime for mandatory climate reporting by certain entities under the Financial Markets Conduct Act.

Key Highlights of the NZ CS

- Purpose: To channel capital toward a low-emissions, climate-resilient future, making climate disclosures integral to investment and business planning.

- Scope: Targets “Climate Reporting Entities” (CREs). This includes major listed companies, banks, insurers, and investment scheme managers. The reporting must start from reporting periods on or after 1 January 2023.

- Framework Structure: Comprises three interlinked standards:

- NZ CS 1 – Core climate related disclosure requirements

- NZ CS 2 – Adoption provisions to ease initial compliance

- NZ CS 3 – General requirements and principles, including materiality and comparability

Detailed Overview of the Three Climate Standards (NZ CS 1, 2, & 3)

NZ CS 1 – Core Disclosure Standards

NZ CS 1 is the central standard that outlines what information must be disclosed. It follows the structure of the Task Force on Climate-related Financial Disclosures (TCFD) and organizes disclosure requirements under four core pillars:

Pillar |

What it Covers |

|---|---|

Governance

|

How the board and management oversee climate-related risks and opportunities. Entities must describe the governance processes in place and their roles.

|

Strategy

|

How climate-related risks and opportunities are integrated into business strategy and financial planning. This includes scenario analysis and assessment of short-, medium-, and long-term impacts.

|

Risk Management

|

Processes for identifying, assessing, and managing climate-related risks. This includes how these processes are integrated into overall risk management frameworks.

|

Metrics and Targets

|

Metrics used to assess climate-related risks, including Scope 1, Scope 2, and Scope 3 greenhouse gas emissions, and the targets set to manage those risks and opportunities.

|

NZ CS 1 requires assurance for reporting periods ending on or after 27 October 2024.

Assurance of greenhouse gas (GHG) emissions reporting under NZ CS 1 is expected to begin from an entity’s second climate statement.

The scope of this assurance engagement will typically include:

- Scope 1, Scope 2, and Scope 3 GHG emissions (You can read about this further in the blog here)

- Additional disclosures required under NZ CS 1, such as:

- The standard(s) used for GHG measurement (e.g. GHG Protocol)

- The consolidation approach applied (equity share, financial control, or operational control)

- Any exclusions of sources, facilities, or operations; along with a clear justification

- Under NZ CS 3, entities must also disclose:

- The methodologies and assumptions used

- Any estimation uncertainty in their emissions data

NZ CS 1 requires entities to obtain at least a limited assurance over their GHG emissions data. However, companies may choose to pursue reasonable assurance for some or all disclosures or voluntarily seek assurance for other non-emissions-related disclosures as well.

What is limited assurance?

A Limited Assurance provides a lower level of confidence. The auditor checks whether anything suggests the information is materially misstated, based on inquiries and analytical procedures. However, this procedure is less detailed than a full audit.

NZ CS 2 – Transitional Guidelines and Reliefs

New Zealand’s Climate Standard 2 (NZ CS 2) provides essential transitional relief to help businesses adjust to new climate reporting requirements. Recognizing that some areas require more time, expertise, or data infrastructure, the standard allows for a phased and practical approach to compliance.

Here’s a breakdown of the key relief provisions and important clarifications:

1. Scenario Analysis (Optional for Non-Financial Entities Initially)

- Relief: Non-financial entities can defer mandatory scenario analysis in the early reporting periods.

- Clarification:

- Financial institutions (e.g., banks, insurers) must still comply with scenario analysis from the start.

- Entities should use this time to build capability for robust scenario modeling in future reports.

2. Scope 3 Emissions (Temporary Omission Permitted)

- Relief: Companies may exclude Scope 3 emissions if they cannot achieve “reasonable assurance” (high confidence in data accuracy).

- Clarification:

- Businesses must still disclose the efforts made to assess Scope 3 and explain why they were omitted.

- This is not a permanent exemption, firms should work toward full disclosure over time.

3. No Comparative Data Required in First Climate Statement

- Relief: The first climate statement does not need to include comparative (prior year) data.

- Clarification:

- From the second year onward, comparative disclosures become mandatory unless exempted.

- This helps reduce early reporting burdens while ensuring progress over time.

NZ CS 3 – Foundational Principles

New Zealand’s Climate Standard 3 (NZ CS 3) serves as the foundational rulebook for climate-related disclosures, ensuring consistency, reliability, and usefulness for investors and stakeholders. Think of it as the “accounting manual” for climate reporting. It sets the principles that govern how entities prepare and present their disclosures under NZ CS 1.

Requirement |

Explanation |

Clarification |

|---|---|---|

Materiality

|

Disclose information that could influence investor decisions about climate risks, opportunities, or financial impacts.

|

Aligns with financial reporting standards (e.g., NZ IFRS). Includes both quantitative (emissions) and qualitative (transition plans) data.

|

Consistency & Comparability

|

Use standardized metrics (e.g., GHG Protocol). Explain methodology changes to maintain comparability.

|

Disclosures must allow comparisons over time (year-to-year) and across entities (industry peers).

|

Fair Presentation & Accuracy

|

Information must be unbiased, complete, and free from material misstatement.

|

Avoid greenwashing; balance risks/opportunities transparently. Disclose limitations or uncertainties.

|

Verifiability

|

Data must be supported by evidence to enable internal/external assurance.

|

Maintain auditable records (e.g., emission calculations). Third-party assurance may be phased in (per NZ CS 2 relief).

|

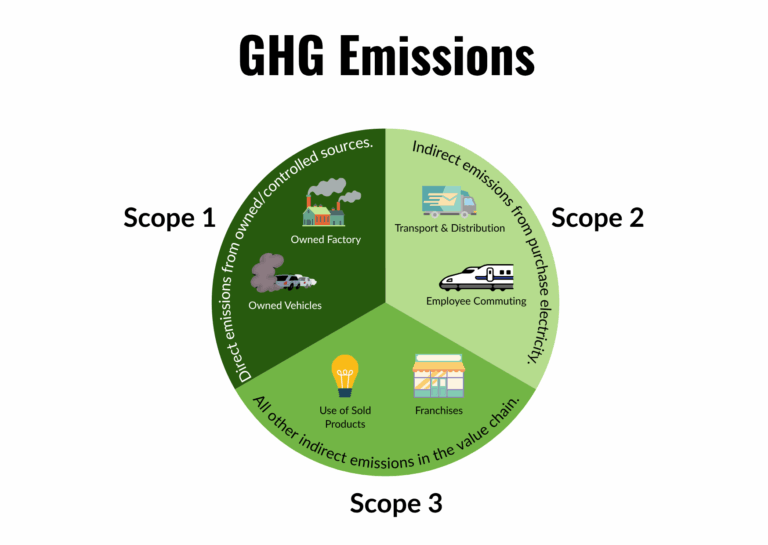

What are Scope 1, 2 & 3 Greenhouse Gas Emissions (GHG)?

Scope 1 – Direct Emissions

Scope 1 emissions are direct GHG emissions that come from sources a company owns or controls.

These typically include:

- Emissions from on-site fuel combustion (e.g. gas boilers, furnaces)

- Emissions from company-owned vehicles (e.g. trucks, vans, service cars)

- Industrial process emissions

Example: A manufacturer running gas-fired machinery on-site would report those emissions as Scope 1.

Scope 2 – Indirect Emissions from Purchased Energy

Scope 2 emissions are indirect emissions from the generation of energy that the company purchases and consumes, such as electricity, steam, heating, or cooling.

Even though the company doesn’t produce these emissions directly, it is responsible for them because it uses the energy.

Under NZ CS 1, entities are expected to disclose location-based and, where available, market-based methods for calculating Scope 2 emissions.

Example: An office that uses grid electricity contributes to emissions at the power plant.

Scope 3 – Other Indirect Emissions from the Value Chain

Scope 3 emissions are all other indirect GHG emissions that occur outside a company’s own operations but are still linked to its activities.

This includes both:

- Upstream activities: e.g. purchased goods and services, transportation, waste, business travel

- Downstream activities: e.g. product use, end-of-life treatment, investments

Scope 3 is typically the largest and most complex category and often makes up the majority of a company’s total carbon footprint.

Example: The emissions from raw materials used by a supplier, or from a customer using a company’s product, fall under Scope 3.

Who Needs to comply to the Aotearoa New Zealand Climate Standards (NZ CS)?

Only Climate Reporting Entities (CREs) are mandated to publish climate-related disclosures and climate statements. These include:

- Large, listed issuers (equity or debt securities) exceeding NZD 60 million in market capitalization or face value

- Registered banks, credit unions, and building societies with total assets over NZD 1 billion

- Licensed insurers with assets over NZD 1 billion or annual premiums over NZD 250 million

- Managers of registered investment schemes (excluding restricted schemes) with assets ≥ NZD 1 billion

- Large Crown financial institutions with AUM over NZD 1 billion

- Overseas businesses operating in New Zealand that meet these thresholds locally

Smaller businesses and SMEs are currently exempt but may still face reporting pressure due to supply chain demands, Scope 3 data requirements, or export compliance needs.

The Aotearoa New Zealand Climate Standards (NZ CS 1–3) establish a clear, structured framework for climate-related disclosures. While compliance is currently mandatory only for large financial entities, the standards reflect a broader shift toward climate transparency in business.

For companies, whether local or international, aligning with these standards is not just about regulation; it’s a strategic move toward climate resilience, investor confidence, and long-term sustainability. French firms looking to partner in New Zealand should understand NZ CS early to stay ahead of both compliance and competitive expectations.